I’ve really been interested in this book for awhile, wondering if it might contain some insight on how to profit from/avoid pain from economic bubbles. (One bubble of particular interest to me is the ongoing Bitcoin/cryptocurrency bubble.) While I could tell the book had lots of good stuff and I did take lots of notes, it was kind of a slog to get through for some reason; and didn’t have much actionable intelligence. Basically, bubbles sometimes “happen for no good reason” (direct quote from the concluding chapter), and then they pop.

Bubble = “a situation in which news of price increases spur investor enthusiasm, which spreads by psychological contagion from person to person, and, in the process, amplifies stories that might justify the price increase and brings in a larger and larger class of investors, who, despite doubts about the real value of the investment, are drawn to it partly through envy of others’ successes and partly through a gambler’s excitement.”

- Big bubble factor is a public impression that a revolution is underway that will change everything (eg. Internet in late 90s; probably Bitcoin today)

- In Shiller’s analysis of large stock market bubbles around the world, the reason for large price increases that often get talked about in media don’t usually make logical sense and there is no actionable pattern. Sometimes there is a kind of bubble feedback going on: a bubble/crash exists only because people think that there is a temporary bubble/crash and want to ride/avoid it

- If we all knew perfectly what our own trading abilities were, there would be no trading: if you were below average, you would never trade because you know you lose most of the time; then the rest would have no one to trade with.

- Market price is by no means a “vote.” Most investors are just trying to follow the perceived “wisdom of the crowd”

- Short sale constraints (such as a limited supply and holders unwilling to lend shares) prolong bubbles, because “smart money” is unable sell down the price. Suggests to Policy makers that bubbles can be overcome by freer and more numerous markets. (Converse: less free, fewer markets = bubble breeder?)

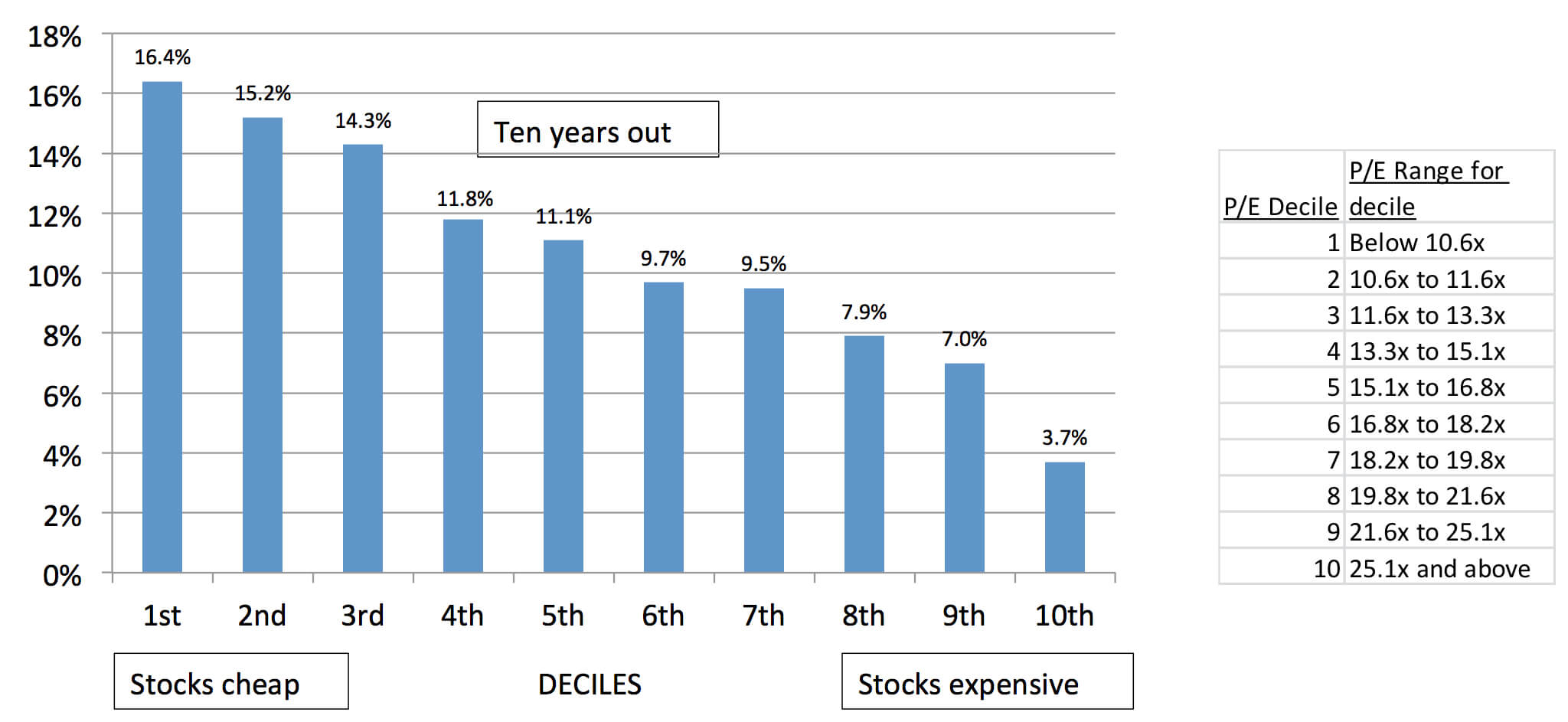

- Higher CAPE can still yield good returns if interest rates low enough

- Ok, I guess there is something actionable: sometimes, you need to ignore pleasant fantasies and defend what you already have.

{kind=link}